Working Group 3 - Chapter 11: Mitigation from a cross-sectoral perspective - (AR4-WG3-11)

Original at: http://www.ipcc.ch/publications_and_data/ar4/wg3/en/ch11.html

Main AR4 Index | Working Group WG3 Index | Table of Contents | Authors | Executive Summary | Annotated Text | References | Reviewer Comments

With the exception of Chapter and Section headings, all coloured text has been inserted by AccessIPCC. The non-coloured text is the IPCC original.

A number of emails from the Climate Research Unit (CRU) of the University of East Anglia were published on the Internet in November 2009. This has provided a window into the world of climate science.

We have identified a number of key individuals involved in the emails whom we have designated as Persons of Concern [PoC]; a Journal in which a PoC has published has been designated as a Journal of Concern [JoC].

This is not to suggest that we believe such papers are necessarily flawed, but rather that, as Joseph Alcamo noted at Bali in October 2009, "as policymakers and the public begin to grasp the multi-billion dollar price tag for mitigating and adapting to climate change, we should expect a sharper questioning of the science behind climate policy".

References occur in a list at the end of each chapter. Citations are within the normal text of sections and paragraphs.

| Tag | Explanation | Where Used | References | Citations |

|---|---|---|---|---|

| PoC |

Person of Concern Key individual involved in CRU emails as defined in this spreadsheet. |

References, Citations, IPCC Roles | 2 | 2 |

| JoC |

Journal of Concern A Journal which has published articles by one or more PoCs (Person of Concern) |

References, Citations | 25 | 25 |

| MoS |

Model or Simulation Reference appears to be a model or simulation, not observation or experiment |

References, Citations | 62 | 104 |

| NPR |

Non Peer Reviewed Reference has no Journal or no Volume or no Pages or it has Editors. |

References, Citations | 142 | 184 |

| SRC |

Self Reference Concern Author of a chapter containing references to own work. |

References, Citations, IPCC Roles | 51 | 66 |

| ARC |

Paper authored or co-authored by person who is also in list of Authors of another chapter. |

References, Citations | 51 | 68 |

| 2007 |

Paper dated 2007, when IPCC policy stated cutoff was December 2005 |

References, Citations | 3 | 4 |

| Ambiguous |

The short inline citation matched with more than one reference; however, AccessIPCC will link to the first reference found. |

Citations | - | 4 |

| NotFound |

The short inline citation was not matched with any reference. Believed to be caused by typing errors. |

Citations | - | 7 |

| Clean |

The reference was probably peer reviewed. |

References, Citations | 78 | 95 |

Coordinating Lead Authors:

Terry Barker (UK) [SRC:6], Igor Bashmakov (Russia) [SRC:1],

| Concern | Occurrence |

|---|---|

| SRC >= 5 | 1 |

| SRC 1-4 | 1 |

| Potentially Biased Authors | 2 |

Lead Authors:

Awwad Alharthi (Saudi Arabia), Markus Amann (Austria) [SRC:4], Luis Cifuentes (Chile) [SRC:2], John Drexhage (Canada), Maosheng Duan (China), Ottmar Edenhofer (Germany) [SRC:3], Brian Flannery (USA), Michael Grubb (UK) [SRC:9], Monique Hoogwijk (Netherlands) [SRC:2], Francis I. Ibitoye (Nigeria), Catrinus J. Jepma (Netherlands), William A. Pizer (USA) [SRC:1], Kenji Yamaji (Japan) [SRC:6],

| Concern | Occurrence |

|---|---|

| SRC >= 5 | 2 |

| SRC 1-4 | 5 |

| Potentially Biased Authors | 7 |

| Impartial Authors | 6 |

Contributing Authors:

Shimon Awerbuch = (USA), Lenny Bernstein (USA), Andre Faaij (Netherlands) [SRC:7], Hitoshi Hayami (Japan), Tom Heggedal (Norway), Snorre Kverndokk (Norway) [SRC:2], John Latham (UK) [SRC:3], Axel Michaelowa (Germany) [SRC:2], David Popp (USA) [SRC:7], Peter Read (New Zealand) [SRC:1], Stefan P. Schleicher (Austria), Mike Smith (UK), Ferenc Toth (Hungary),

| Concern | Occurrence |

|---|---|

| SRC >= 5 | 2 |

| SRC 1-4 | 4 |

| Potentially Biased Authors | 6 |

| Impartial Authors | 7 |

Review Editors:

David Hawkins (USA), Aviel Verbruggen (Belgium),

| Concern | Occurrence |

|---|---|

| Impartial Authors | 2 |

This chapter should be cited as:

Barker, T., I. Bashmakov, A. Alharthi, M. Amann, L. Cifuentes, J. Drexhage, M. Duan, O. Edenhofer, B. Flannery, M. Grubb, M. Hoogwijk, F. I. Ibitoye, C. J. Jepma, W.A. Pizer, K. Yamaji, 2007: Mitigation from a cross-sectoral perspective. In Climate Change 2007: Mitigation. Contribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change [B. Metz, O.R. Davidson, P.R. Bosch, R. Dave, L.A. Meyer (eds)], Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

EXECUTIVE SUMMARY

Mitigation potentials and costs from sectoral studies

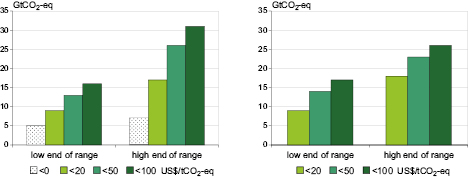

The economic potentials for GHG mitigation at different costs have been reviewed for 2030 on the basis of bottom-up studies. The review confirms the Third Assessment Report (TAR) finding that there are substantial opportunities for mitigation levels of about 6 GtCO2-eq involving net benefits (costs less than 0), with a large share being located in the buildings sector. Additional potentials are 7 GtCO2-eq at a unit cost (carbon price) of less than 20 US$/tCO2-eq, with the total, low-cost, potential being in the range of 9 to 18 GtCO2-eq. The total range is estimated to be 13 to 26 GtCO2-eq, at a cost of less than 50 US$/tCO2-eq and 16 to 31 GtCO2-eq at a cost of less than 100 US$/tCO2-eq (370 US$/tC-eq). As reported in Chapter 3 , these ranges are comparable with those suggested by the top-down models for these carbon prices by 2030, although there are differences in sectoral attribution (medium agreement, medium evidence).

No one sector or technology can address the entire mitigation challenge. This suggests that a diversified portfolio is required based on a variety of criteria. All the main sectors contribute to the total. In the lower-cost range, and measured according to end-use attribution, [1] the potentials for electricity savings are largest in buildings and agriculture. When attribution is based on point of emission, [2] energy supply makes the largest contribution (high agreement, much evidence).

These estimated ranges reflect some key sensitivities to baseline fossil fuel prices (most studies use relatively low fossil fuel prices) and discount rates. The estimates are derived from the underlying literature, in which the assumptions adopted are not usually entirely comparable and where the coverage of countries, sectors and gases is limited.

Bioenergy

These estimates assume that bioenergy options will be important for many sectors by 2030, with substantial growth potential beyond, although no complete integrated studies are available for supply-demand balances. The usefulness of these options depends on the development of biomass capacity (energy crops) in balance with investments in agricultural practices, logistic capacity, and markets, together with the commercialization of second-generation biofuel production. Sustainable biomass production and use imply the resolution of issues relating to competition for land and food, water resources, biodiversity and socio-economic impact.

Unconventional options

The aim of geo-engineering options is to remove CO2 directly from the air, for example through ocean fertilization, or to block sunlight. However, little is known about effectiveness, costs or potential side-effects of the options. Blocking sunlight does not affect the expected escalation in atmospheric CO2 levels, but could reduce or eliminate the associated warming. Disconnecting CO2 concentration and global temperature in this way could induce other effects, such as the further acidification of the oceans (medium agreement, limited evidence).

Carbon prices and macro-economic costs of mitigation to 2030

Diverse evidence indicates that carbon prices in the range 20–50 US$/tCO2 (US$75–185/tC), reached globally by 2020 – 2030 and sustained or increased thereafter, would deliver deep emission reductions by mid-century consistent with stabilization at around 550ppm CO2-eq (Category III levels, see Table 3.10 ) if implemented in a stable and predictable fashion. Such prices would deliver these emission savings by creating incentives large enough to switch ongoing investment in the world’s electricity systems to low-carbon options, to promote additional energy efficiency, and to halt deforestation and reward afforestation. [3] For purposes of comparison, it can be pointed out that prices in the EU ETS in 2005 – 2006 varied between 6 and 40 US$/tCO2. The emission reductions will be greater (or the price levels required for a given trajectory lower in the range indicated) to the extent that carbon prices are accompanied by expanding investment in technology RD&D and targeted market-building incentives (high agreement, much evidence).

Pathways towards 650ppm CO2-eq (Category IV levels; see Table 3.10 ) could be compatible with such price levels being deferred until after 2030 . Studies by the International Energy Agency suggest that a mid-range pathway between Categories III and IV, which returns emissions to present levels by 2050, would require global carbon prices to rise to 25 US$/tCO2 by 2030 and be maintained at this level along with substantial investment in low-carbon energy technologies and supply (high agreement, much evidence).

Effects of the measures on GDP or GNP by 2030 vary accordingly (and depend on many other assumptions). For the 650ppm CO2-eq pathways requiring reductions of 20% global CO2 or less below baseline, those modelling studies that allow for induced technological change involve lower costs than the full range of studies reported in Chapter 3 , depending on policy mix and incentives for the innovation and deployment of low-carbon technologies. Costs for more stringent targets of 550 ppm CO2-eq requiring 40% CO2 abatement or less show an even more pronounced reduction in costs compared to the full range (high agreement, much evidence).

Mitigation costs depend critically on the baseline, the modelling approaches and the policy assumptions. Costs are lower with low-emission baselines and when the models allow technological change to accelerate as carbon prices rise. Costs are reduced with the implementation of Kyoto flexibility mechanisms over countries, gases and time. If revenues are raised from carbon taxes or emission schemes, costs are lowered if the revenues provide the opportunity to reform the tax system, or are used to encourage low-carbon technologies and remove barriers to mitigation (high agreement, much evidence).

Innovation and costs

All studies make it clear that innovation is needed to deliver currently non-commercial technologies in the long term in order to stabilize greenhouse gas concentrations (high agreement, much evidence).

A major development since the TAR has been the inclusion in many top-down models of endogenous technological change. Using different approaches, modelling studies suggest that allowing for endogenous technological change reduces carbon prices as well as GDP costs, this in comparison with those studies that largely assumed that technological change was independent of mitigation policies and action. These reductions are substantial in some studies (medium agreement, limited evidence).

Attempts to balance emission reductions equally across sectors (without trading) are likely to be more costly than an approach primarily guided by cost efficiency. Another general finding is that costs will be reduced if policies that correct the two relevant market failures are combined by incorporating the damage resulting from climate change in carbon prices, and the benefits of technological innovation in support for low-carbon innovation. An example is the recycling of revenues from tradeable permit auctions to support energy efficiency and low-carbon innovations. Low-carbon technologies can also diversify technology portfolios, thereby reducing risk (high agreement, much evidence).

Incentives and investment

The literature emphasizes the need for a range of cross-sectoral measures in addition to carbon pricing, notably in relation to regulatory and behavioural aspects of energy efficiency, innovation, and infrastructure. Addressing market and regulatory failures surrounding energy efficiency, and providing information and support programmes can increase responsiveness to price instruments and also deliver direct emission savings (high agreement, much evidence).

Innovation may be greatly accelerated by direct measures and one robust conclusion from many reviews is the need for public policy to promote a broad portfolio of research. The literature also emphasizes the need for a range of incentives that are appropriate to different stages of technology development, with multiple and mutually supporting policies that combine technology push and pull in the various stages of the ‘innovation chain’ from R&D through the various stages of commercialization and market deployment. In addition, the development of cost-effective technologies will be rewarded by well-designed carbon tax or cap and trade schemes through increased profitability and deployment. Even so, in some cases, the short-term market response to climate policies may lock in existing technologies and inhibit the adoption of more fruitful options in the longer term (high agreement, much evidence).

Mitigation is not a discrete action: investment, in higher or lower carbon options, is occurring all the time. The estimated investment required is around $20 trillion in the energy sector alone out to 2030 . Many energy sector and land use investments cover several decades; buildings, urban and transport infrastructure, and some industrial equipment may influence emission patterns over the century. Emission trajectories and the potential to achieve stabilization levels, particularly in Categories A and B, will be heavily influenced by the nature of these investments. Diverse policies that deter investment in long-lived carbon-intensive infrastructure and reward low-carbon investment could maintain options for these stabilization levels at lower costs (high agreement, much evidence).

However, current measures are too uncertain and short-term to deliver much lower-carbon investment. The perceived risks involved mean that the private sector will only commit the required finance if there are incentives (from carbon pricing and other measures) that are clearer, more predictable, longer-term and more robust than provided for by current policies (high agreement, much evidence).

Spillover effects from Annex I action

Estimates of carbon leakage rates for action under Kyoto range from 5 to 20% as a result of a loss of price competitiveness, but they remain very uncertain. The potential beneficial effect of technology transfer to developing countries arising from technological development brought about by Annex I action may be substantial for energy-intensive industries. However, it has not yet been quantified reliably. As far as existing mitigation actions, such as the EU ETS, are concerned, the empirical evidence seems to indicate that competitive losses are not significant, confirming a finding in the TAR (medium agreement, limited evidence).

Perhaps one of the most important ways in which spillover from mitigation action in one region affects others is through its effect on world fossil fuel prices. When a region reduces its local fossil fuel demand as a result of mitigation policy, it will reduce world demand for that commodity and so put downward pressure on prices. Depending on the response from fossil-fuel producers, oil, gas or coal prices may fall, leading to loss of revenue for the producers, and lower costs of imports for the consumers. Nearly all modelling studies that have been reviewed indicate more pronounced adverse effects on countries with high shares of oil output in GDP than on most of the Annex I countries taking abatement action (high agreement, much evidence).

Co-benefits of mitigation action

Co-benefits of action in the form of reduced air pollution, more energy security or more rural employment offset mitigation costs. While the studies use different methodological approaches, there is general consensus for all world regions analyzed that near-term health and other benefits from GHG reductions can be substantial, both in industrialized and developing countries. However, the benefits are highly dependent on the policies, technologies and sectors chosen. In developing countries, much of the health benefit could result from improvements in the efficiency of, or switching away from, the traditional use of coal and biomass. Such near-term co-benefits of GHG control provide the opportunity for a true no-regrets GHG reduction policy in which substantial advantages accrue even if the impact of human-induced climate change itself turns out to be less than that indicated by current projections (high agreement, much evidence).

Adaptation and mitigation from a sectoral perspective

Mitigation action for bioenergy and land use for sinks are expected to have the most important implications for adaptation. There is a growing awareness of the unique contribution that synergies between mitigation and adaptation could provide for the rural poor, particularly in the least developed countries: many actions focusing on sustainable policies for managing natural resources could provide both significant adaptation benefits and mitigation benefits, mostly in the form of carbon sink enhancement (high agreement, limited evidence).

11.1 Introduction

This chapter takes a cross-sectoral approach to mitigation options and costs, and brings together the information in Chapters 4 to 10 to assess overall mitigation potential. It compares these sectoral estimates with the top-down estimates from Chapter 3 , adopting a more short- and medium-term perspective, taking the assessment to 2030 . It assesses the cross-sectoral and macro-economic cost literatures since the Third Assessment Report (TAR) ( IPCC, 2001 [NPR] ), and those covering the transition to a low-carbon economy, spillovers and co-benefits of mitigation.

The chapter starts with an overview of the cross-cutting options for mitigation policy ( Section 11.2 ), including technologies that cut across sectors, such as hydrogen-based systems and options not covered in earlier chapters, examples being ocean fertilization, cloud creation and bio- and geo-engineering. Section 11.3 covers overall mitigation potential by sector, bringing together the various options, presenting the assessment of the sectoral implications of mitigation, and comparing bottom-up with top-down estimates. Section 11.4 covers the literature on the macro-economic costs of mitigation.

Since the TAR, there is much more literature on the quantita-tive implications of introducing endogenous technological change into the models. Many studies suggest that higher carbon prices and other climate policies will accelerate the adoption of low-carbon technologies and lower macroeconomic costs, with estimates ranging from a negligible amount to negative costs (net benefits). Section 11.5 describes the effects of introducing endogenous technological change into the models, and particularly the effects of inducing technological change through climate policies.

The remainder of the chapter looks at interactions of various kinds: Section 11.6 links the medium-term to the long-term issues discussed in Chapter 3 , linking the shorter-term costs and social prices of carbon to the longer-term stabilization targets; 11.7 covers spillovers from action in one group of countries on the rest of the world; 11.8 covers co-benefits (particularly local air quality benefits) and costs; and 11.9 deals with synergies and trade-offs between mitigation and adaptation.

11.2 Technological options for cross-sectoral mitigation: description and characterization

This section covers technologies that affect many sectors (11.2.1) and other technologies that cannot be attributed to any of the sectors covered in Chapters 4 to 10 (geo-engineering options etc. in 11.2.2). The detailed consolidation and synthesis of the mitigation potentials and costs provided in Chapters 4 to 10 are covered in the next section, 11.3.

11.2.1 Cross-sectoral technological options

Cross-sectoral mitigation technologies can be broken down into three categories in which the implementation of the technology:

1. occurs in parallel in more than one sector;

2. could involve interaction between sectors, or

3. could create competition among sectors for scarce resources.

Some of the technologies implemented in parallel have been discussed earlier in this report. Efficient electric motor-driven systems are used in the industrial sector ( Section 7.3.2 ) and are also a part of many of the technologies for the buildings sector, e.g. efficient heating, ventilation and air conditioning systems ( Section 6.4.5 ). Solar PV can be used in the energy sector for centralized electricity generation ( Section 4.3.3.6 ) and in the buildings sector for distributed electricity generation ( Section 6.4.7 ). Any improvement in these technologies in one sector will benefit the other sectors.

On a broad scale, information technology (IT) is imple-mented in parallel across sectors as a component of many end-use technologies, but the cumulative impact of its use has not been analyzed. For example, IT is the basis for integrating the control of various building systems, and has the potential to reduce building energy consumption ( Section 6.4.6 ). IT is also the key to the performance of hybrids and other advanced vehicle technologies ( Section 5.3.1.2 ). Smart end-use devices (household appliances, etc) could use IT to program their operation at times when electricity demand is low. This could reduce peak demand for electricity, resulting in a shift to base load generation, which is usually more efficient ( Hirst, 2006 [NPR] ). The impact of such a switch on CO2 emissions is unknown, because it is easy to construct cases where shifts from peak load to base load would increase CO2 emissions (e.g., natural-gas-fired peak load, but coal-fired base load). General improvements in IT, e.g. cheaper computer chips, will benefit all sectors, but applications have to be tailored to the specific end-use. Of course, the net impact of IT on greenhouse gas emissions could result either in net reductions or gains, depending for example on whether or not efficiency gains are offset by increases in production.

An example of a group of technologies that could involve interaction between sectors is gasification/hydrogen/carbon dioxide capture and storage (CCS) technology ( IPCC, 2005 [NPR] and Chapter 4 .3.6). While these technologies can be discussed separately, they are interrelated and being applied as a group enhances their CO2-emission mitigation potential. For example, CCS can be applied as a post-combustion technology, in which case it will increase the amount of resource needed to generate a unit of heat or electricity. Using a pre-combustion approach, i.e. gasifying fossil fuels to produce hydrogen that can be used in fuel cells or directly in combustion engines, may improve overall energy efficiency. However, unless CCS is used to mitigate the CO2 by-product from this process, the use of that hydrogen will offer only modest benefits. (See Section 5.3.1.4 for a comparison of fuel cell and hybrid vehicles.) Adding CCS would make hydrogen an energy carrier, providing a low CO2 emission approach for transportation, buildings, or industrial applications. Implementation of fuel cells in stationary applications could provide valuable learning for vehicle application; in addition, fuel cell vehicles could provide electric power to homes and buildings ( Romeri, 2004 [NPR] ).

In the longer term, hydrogen could be manufactured by gasifying biomass – an approach which has the potential to achieve negative CO2 emissions ( IPCC, 2005 [NPR] ) – or through electrolysis using carbon-free sources of electricity, a zero CO2 option. In the even longer term, it may be possible to produce hydrogen by other processes, e.g. biologically, using genetically-modified organisms ( GCEP, 2005 [NPR] ). However, none of these longer-term technologies are likely to have a significant impact before 2030, the time frame for this analysis.

Biomass is an example of a cross-sectoral technology which may compete for resources. Any assessment of the use of biomass, e.g., as a source of transportation fuels, must consider competing demands from other sectors for the creation and utilization of biomass resources. Technical breakthroughs could allow biomass to make a larger future contribution to world energy needs. Such breakthroughs could also stimulate the investments required to improve biomass productivity for fuel, food and fibre. See Chapter 4 and Section 11.3 .

Another example of resource competition involves natural gas. Natural gas availability could limit the application of some short- to medium-term mitigation technology. Switching to lower carbon fuels, e.g. from coal to natural gas for electricity generation, or from gasoline or diesel to natural gas for vehicles, is a commonly cited short-term option. Because of its higher hydrogen content, natural gas is also the preferred fossil fuel for hydrogen manufacture. Discussion of these options in one sector rarely takes natural gas demand from other sectors into account.

In conclusion, there are several important interactions between technologies across sectors that are seldom taken into account. This is an area of energy system modelling that requires further investigation.

11.2.2 Ocean fertilization and other geo-engineering options

Since the TAR, a body of literature has developed on alternative, geo-engineering techniques for mitigating climate change. This section focuses on apparently promising techniques: ocean fertilization, geo-engineering methods for capturing and safely sequestering CO2 and reducing the amount of sunlight absorbed by the earth’s atmospheric system. These options tend to be speculative and many of their environmental side-effects have yet to be assessed; detailed cost estimates have not been published; and they are without a clear institutional framework for implementation. Conventional carbon capture and storage is covered in Chapter 4 , Section 4.3.6 and the IPCC Special Report ( 2005 ) on the topic.

11.2.2.1 Iron and nitrogen fertilization of the oceans

Iron fertilization of the oceans may be a strategy for removing CO2 from the atmosphere. The idea is that it stimulates the growth of phytoplankton and therefore sequesters CO2 in the form of particulate organic carbon (POC). There have been eleven field studies in different ocean regions with the primary aim of examining the impact of iron as a limiting nutrient for phytoplankton by the addition of small quantities (1–10 tonnes) of iron sulphate to the surface ocean. In addition, commercial tests are being pursued with the combined (and conflicting) aims of increasing ocean carbon sequestration and productivity. It should be noted, however, that iron addition will only stimulate phytoplankton growth in ~30% of the oceans (the Southern Ocean, the equatorial Pacific and the Sub-Arctic Pacific), where iron depletion prevails. Only two experiments to date ( Buesseler and Boyd, 2003 [JoC] ) have reported on the second phase, the sinking and vertical transport of the increased phytoplankton biomass to depths below the main thermocline (>120m). The efficiency of sequestration of the phytoplankton carbon is low (<10%), with the biomass being largely recycled back to CO2 in the upper water column ( Boyd et al., 2004 [JoC] ). This suggests that the field-study estimates of the actual carbon sequestered per unit iron (and per dollar) are over-estimates. The cost of large-scale and long-term fertilization will also be offset by CO2 release/emission during the acquisition, transportation and release of large volumes of iron in remote oceanic regions. Potential negative effects of iron fertilization include the increased production of methane and nitrous oxide, deoxygenation of intermediate waters and changes in phytoplankton community composition that may cause toxic blooms and/or promote changes further along the food chain. None of these effects have been directly identified in experiments to date, partly due to the time and space constraints.

Nitrogen fertilization is another option ( Jones, 2004 [NPR] ) with similar problems and consequences.

11.2.2.2 Technologically-varied solar radiative forcing

The basic principle of these technologies is to reduce the amount of sunlight accepted by the earth’s system by an amount sufficient to compensate for the heating resulting from enhanced atmospheric CO2 concentrations. For CO2 levels projected for 2100, this corresponds to a reduction of about 2%. Three techniques are considered:

A. Deflector System at Earth-Sun L-1 [4] point. The principle underlying this idea (e.g. Seifritz 1989 [JoC] Teller et al. 2004 [NPR] Angel 2006 [NPR] )) is to install a barrier to sunlight measuring about 106 km2 at or close to the L-1 point. Teller et al. estimate that its mass would be about 3000 t, consisting of a 30µm metallic screen with 25nm ribs. [5] They envisage it being spun in situ, and emplaced by one shuttle flight a year over 100 years. It should have essentially zero maintenance. The cost has not yet been determined. Computations by ( Govindasamy et al. 2003 ) ) suggest that this scheme could markedly reduce regional and seasonal climate change.

B. Stratospheric Reflecting Aerosols. This technique involves the controlled scattering of incoming sunlight with airborne sub-microscopic particles that would have a stratospheric residence time of about 5 years. Teller et al. 2004 [NPR] ) suggest that the particles could be: (a) dielectrics; (b) metals; (c) resonant scatterers. Crutzen 2006 [JoC] ) proposes (d) sulphur particles. The implications of these schemes, particularly with regard to stratospheric chemistry, feasibility and costs, require further assessment ( Cicerone, 2006 [JoC] ).

C. Albedo Enhancement of Atmospheric Clouds. This scheme ( Latham, 1990 [JoC, SRC] ; 2002 ) involves seeding low-level marine stratocumulus clouds – which cover about a quarter of the Earth’s surface – with micrometre-sized aerosol, formed by atomizing seawater. The resulting increases in droplet number concentrations in the clouds raises cloud albedo for incoming sunlight, resulting in cooling which could be controlled ( Bower et al., 2006 [SRC] ) and be sufficient to compensate for global warming. The required seawater atomization rate is about 10 m3/sec. The costs would be substantially less than for the techniques mentioned under B. An advantage is that the only raw material required is seawater but, while the physics of this process are reasonably well understood, the meteorological ramifications need further study.

These schemes do not affect the expected escalation in atmospheric CO2 levels, but could reduce or eliminate the associated warming. Disconnecting CO2 concentration and global temperature in this way could have beneficial consequences such as increases in the productivity of agri- culture and forestry. However, there are also risks and this approach will not mitigate or address other effects such as increasing ocean acidification (see IPCC, 2007b [NPR, 2007] , Section 4.4.9).

11.3 Overall mitigation potential and costs, including portfolio analysis and cross-sectoral modelling

This section synthesizes and aggregates the estimates from chapters 4 to 10 and reviews the literature investigating cross-sectoral effects. The aim is to identify current knowledge about the integrated mitigation potential and/or costs covering more than two sectors. There are many specific policies for reducing GHG emissions (see Chapter 13 ). Non-climate policies may also yield substantial GHG reductions as co-benefits (see Section 11.8 and Chapter 12 ). All these policies have direct sectoral effects. They also have indirect cross-sectoral effects, which are covered in this section and which diffuse across countries. For example, domestic policies promoting a new technology to reduce the energy use of domestic lighting lead to reductions in emissions of GHG from electricity generation. They may also result in more exports of the new technology and, potentially, additional energy savings in other countries. This section also looks at studies relating to a portfolio analysis of mitigation options.

11.3.1 Integrated summary of sectoral emission potentials

Chapters 4 to 10 assessed the economic potential of GHG mitigation at a sectoral scale for the time frame out to 2030 (for a discussion of the different definitions of potential, see Chapter 2 ). These bottom-up estimates are derived using a variety of literature sources and various methodologies, as discussed in the underlying chapters. This section derives ranges of aggregate economic potentials for GHG mitigation over different costs (i.e. carbon prices) at year- 2000 prices.

11.3.1.1 Problems in aggregating emissions

In compiling estimates of this kind, various issues must be considered:

Comparability: There is no common, standardized approach in the underlying literature that is used systematically for assessing the mitigation potential. The comparability of data is therefore far from perfect. The comparability problem was addressed by using a common format to bring together the variety of data found in the literature (as shown below in section 11.3.1.3 and Table 11.3 ), acknowledging that any aberrations due to a lack of a common methodological base may in part cancel each other out in the aggregation process. Some extrapolations were necessary, for example in the residential sector where the literature mostly refers to 2020 . The final result can be considered the best result that is possible and it is accurate within the uncertainty ranges provided.

Coverage: Chapters 4 to 10 together cover virtually all sources of greenhouse gas emissions. However, for parts of some sectors, it was not possible to derive emission reduction potentials from the literature. Furthermore, no quantified emission reduction potentials were available for some options. This leads to a certain under-estimation of the emission reduction potential as discussed in Section 11.3.1.3 . The under-estimation of the total mitigation potential is limited, but not negligible.

Baselines: Ideally, emission reduction potentials should adopt a common baseline. Some emission scenarios, such as those developed for the Special Report on Emission Scenarios ( IPCC, 2000 [NPR] ), are suitable for worldwide, sectoral and multi-gas coverage. However, for a number of sectors, such baselines are not detailed enough to serve as a basis for making bottom-up emission reduction calculations. The baselines used are described and discussed further in Section 11.3.1.2 .

Aggregation: The aggregation of mitigation potentials for various sectors is complicated by the fact that mitigation action in one sector may affect mitigation potential in another. There is a risk of double counting of potentials. The problem and the procedures used to overcome this risk are explained in Section 11.3.1.3 . In addition the baselines differ to some extent.

11.3.1.2 The baseline

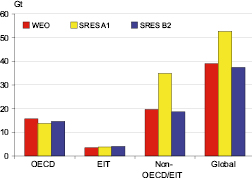

All mitigation potentials have to be estimated against a baseline. The main baseline scenarios used for compiling the assessments in the chapters are the SRES B2 and A1B marker scenarios ( IPCC, 2000 [NPR] ) and the World Energy Outlook 2004 (WEO 2004 ( IEA, 2004 [NPR] ). The assumed emissions in the three baseline scenarios vary in magnitude and regional distribution. The baseline scenarios B2 and WEO 2004 are comparable in the main assumptions for population, GDP and energy use. Figure 11.1 shows that the emissions are also comparable. Scenario A1B, which assumes relatively higher economic growth, shows substantially higher emissions in countries outside the OECD/EIT region.

Figure 11.1: Energy-related CO2-only emissions per world region for the year 2030 in the World Energy Outlook, and in the SRES B2 and A1B scenarios

The crude oil prices assumed in SRES B2 and WEO 2004 are of the same order of magnitude. The oil prices in the SRES scenarios vary across studies. For the MESSAGE model (B2 scenario), the price is about 25 US$/barrel ( Riahi et al., 2006 [NPR, MoS, ARC] ). In the case of the WEO 2004, for example, the oil price assumed in 2030 is 29 US$/barrel. These prices (and all other energy price assumptions) are substantially lower than those prevailing in 2006 and assumed for later projections ( IEA, 2005 [NPR] and 2006b ). The 2002 –6 rises in world energy prices are also reflected in the energy futures markets for at least another five to ten years. In fact, the rise in crude oil prices during this period, some 50 US$/barrel, is comparable to the impact of a 100 US$/tCO2-eq increase in the price of carbon. However, it is still uncertain whether these price increases will have a significant impact on the long-term energy price trend.

Higher energy prices and further action on mitigation may reinforce each other in their impact on mitigation potential, although it is still uncertain how and to what extent. On the one hand, for instance, economies of scale may facilitate the introduction of some new technologies if supported by a higher energy price trend. On the other hand, it is also conceivable that, once some cost-effective innovation has already been triggered by higher energy prices, any further mitigation action through policies and measures may become more costly and difficult. Finally, although general energy prices rises will encourage energy efficiency, the mix of the different fuel prices is also important. Oil and gas prices have risen substantially in relation to coal prices 2002 –6, and this will encourage greater use of coal, for example in electricity generation, increasing GHG emissions.

As a rule, the SRES B2 and WEO 2004 baselines were both used for the synthesis of the emission mitigation potentials by sector. Most chapters have reported the mitigation potential for at least one of these baseline scenarios. There are a few exceptions. Chapter 5 (transportation) uses a different, more suitable, scenario ( WBCSD, 2004 [NPR] ). However, it is comparable to WEO 2004 . Chapter 6 (buildings) constructed a baseline scenario with CO2 emissions between those of the SRES B2 and A1B marker scenarios taken from the literature (see Section 6.5 ). The agriculture and forestry sectors based their mitigation potential on changes in land use as deduced from various scenarios (including marker scenarios, see Sections 8.4.3 and 9.4.3 ). The SRES scenarios did not include enough detail for the waste sector, so Chapter 10 used the GDP and population figures from SRES A1B and the methodologies described in IPCC Guidelines 2006 (see Section 10.4.7 ).

Table 11.1 compares the emissions of the different sectoral baselines for 2004 and 2030 against a background of the end-use and point-of-emission allocation of emissions attributed to electricity use. Since the 2030 data are from studies that differ in terms of coverage and comparability, they should not be directly aggregated across the different sectors and therefore no totals across all sectors are shown in Table 11.16 . An important difference between the WEO baseline and SRES B2 is that the WEO emissions do not include all non-CO2 GHG emissions.

Table 11.1: Overview of the global emissions for the year 2004 and the baseline emissions for all GHGs adopted for the year 2030 (in GtCO2-eq)

| Global emissions 2004 (allocated to the end-use sector)a, c | Global emissions 2004 (point of emissions)a, b | Type of baseline usedd | Global emissions 2030 (allocated to the end-use sector) | Global emissions 2030 (point of emissions) | |

|---|---|---|---|---|---|

| Energy supply | - j | 12.7 | WEO | - j, f) | 15.8 f) |

| Transport | 6.4 | 6.4 | WEO | 10.6 f) | 10.6 f) |

| Buildings | 9.2 | 3.9 | Own | 14.3 f) | 5.9 e) f) |

| Industry | 12.0 | 9.5 | B2/USEPA | 14.6 | 8.5 g) |

| Agriculture | 6.6 | 6.6 | B2/FAO | 8.3 | 8.3 |

| LULUCF/Forestryk) | 5.8 | 5.8 | Own | 5.8 h) | 5.8 h) |

| Wastei) | 1.4 | 1.4 | A1B | 2.1 | 2.1 |

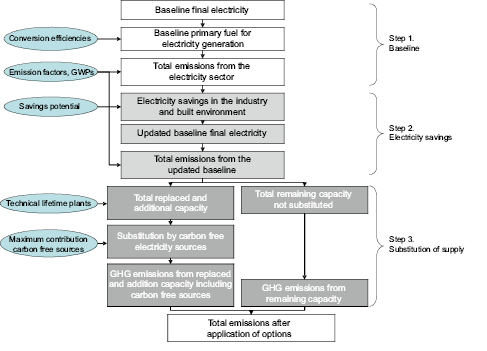

11.3.1.3 Synthesizing the potentials from Chapters 4 to 10 involving electricity

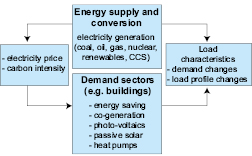

When aggregating the sectoral mitigation potentials, the links between sectors need to be considered ( Figure 11.2 ). For example, the options in electricity supply interact with those for electricity demand in the buildings and industry sectors. On the supply side, fossil-fuel electricity can be substituted by low-CO2 or CO2-free technologies such as renewable sources, nuclear energy, bioenergy or fossil fuel in combination with carbon capture and storage. On the demand side, the buildings and the industrial sectors have options for electricity savings. The emission reductions from these two sets of options cannot be aggregated since emission reductions in demand reduce the potential for those in supply and vice-versa.

To overcome this problem, the following approach was adopted: The World Energy Outlook ( IEA, 2004 [NPR] ) for the year 2030 was used as the baseline. The potentials from electricity savings in the buildings and the industry sectors were estimated first. Electricity savings then reduce demand for electricity. This sequence was followed because electricity savings can be achieved at relatively low cost and their implementation can therefore be expected first. Electricity savings were converted to emission reductions using the average carbon intensity of the electricity supply in the baseline for the year 2030 . In reality, it can be expected that electricity savings would result in a relatively larger reduction in fossil-fuel electricity generation than electricity generation involving low marginal costs such as renewables and nuclear. This is because, in the operating system, low-cost generation is normally called on before high-cost generation. However, this response depends on local conditions and it is not appropriate to consider it here. However, it does imply that the emission reductions for electricity savings reported here are an under-estimate. This under-estimate becomes more pronounced with higher carbon prices, and higher marginal costs for fossil fuels.

The detailed sequence is as follows:

1. Electricity savings from the measures in the buildings and industry sector were subtracted from the baseline supply estimates to obtain the corrected electricity supply for 2030 .

2. No early withdrawal of plant or stranded assets is assumed. Low-carbon options can therefore only be applied to new electricity supply.

3. The new electricity supply required to 2030 was calculated from 1) additional new capacity between 2010 and 2030 and 2) capacity replaced in the period 2010 – 2030 after an assumed average plant lifetime of 50 years (see Chapter 4.4.3).

4. The new electricity supply required was divided between available low-carbon supply options. As the cost estimates were lowest for a fuel switch from coal to natural gas supply, it was assumed that this would take place first. In accordance with Chapter 4 it was assumed that 20% of the new coal plants required would be substituted by gas technologies.

5. An assessment was made of the prevented emissions from the other low-carbon substitution options after the fuel switch. The following technologies were taken into account: renewables (wind and geothermal), bioenergy, hydro, nuclear and CCS. It was assumed that the fossil fuel requirement in the baseline (after adjustments for the previous step) was met by these low-carbon intensive technologies. The substitution was made on the basis of relative maximum technical potential. The same breakdown as in Section 4.4.3 was used for the low-carbon options.

6. It was then possible to estimate the resulting mitigation potential for the energy sector, after savings in the end-use sectors buildings and industry.

7. For the buildings and industry sectors, the mitigation potential was broken down into emission savings resulting from less electricity use and the remainder.

8. For sectors other than energy, buildings and industry, the data given in the chapters were used for the overall aggregation.

When evaluating mitigation potential in the energy supply sector, the calculations in Chapter 4 did not subtract the electricity savings from the buildings and industry sectors (see Chapter 4 , Table 4.19 ). Adopting this order (which is not the preferred order, as explained above) implies first taking all the mitigation measures in the energy sector and then applying the electricity savings from buildings and industry sectors. This would result in different mitigation potentials for each of the sectors and mitigation measures, although the total will not change. See Appendix 11.1 for a further discussion of the methodology and details of the calculation.

In the case of the other sectors, the data given in the chapters were used for the overall aggregation. The mitigation potential for the buildings and industry sectors was broken down into emission savings for lower electricity use and the remainder, so that the potential could be re-allocated where necessary to the power sector.

11.3.1.4 Synthesizing the potentials from Chapters 4 to 10 involving biomass

Biomass supplies originate in agriculture (residues and cropping), forestry, waste supplies, and in biomass processing industries (such as the paper & pulp and sugar industries). Key applications for biomass are conversion to heat, power, transportation fuels and biomaterials. Information about biomass supplies and utilization is distributed over the relevant chapters in this report and no complete integrated studies are available for biomass supply-demand balances and biomass potential.

Biomass demand from different sectors

Demand for biomass as transportation fuel involves the production of biofuels from agricultural crops such as sugar cane, rape seed, corn, etc., as well as potentially ‘second-generation’ biofuels produced from lignocellulosic biomass. The first category dominates in the shorter term. The penetration of second-generation biofuels depends on the speed of technological development and the market penetration of gasification technology for synfuels and hydrolysis technology for the production of ethanol from woody biomass. Demand projections for primary biomass in Chapter 5 are largely based on WEO-IEA ( 2006 ) global projections, with a relatively wide range of about 14 to 40 EJ of primary biomass, or 8–25 EJ of fuel. However, there are also higher estimates ranging from 45 to 85 EJ demand for primary biomass in 2030 (or roughly 30–50 EJ of fuel) (see Chapter 5 ).

Demand for biomass for power and heat is considered in Chapter 4 (energy). Demand for biomass for heat and power will be strongly influenced by the availability and introduction of competing technologies such as CCS, nuclear power, wind energy, solar heating, etc. The projected demand in 2030 for biomass would be around 28–43 EJ according to the data used in Section 4.4.3.3 . These estimates focus on electricity generation. Heat is not explicitly modelled or estimated in the WEO, resulting in an under-estimate of total demand for biomass.

Industry is an important user of biomass for energy, most notably the paper & pulp industry and the sugar industry, which both use residues for generating process energy (steam and electricity). Chapter 7 highlights improvements in energy production from such residues, most notably the deployment of efficient gasification/combined cycle technology that could strongly improve efficiencies in, for example, pulp and sugar mills. Mitigation potentials reducing the demand for such commodities or raising the recycling rate for paper will not result in additional biomass demand. Biomass can also be used for the production of chemicals and plastics, and as a reducing agent for steel production (charcoal) and for construction purposes (replacing, for example, metals or concrete). Projections for such production routes and subsequent demand for biomass feedstocks are not included in this report, since their deployment is expected to be very limited (see Chapter 7 ).

In the built environment, biomass is used in particular for heating for both non-commercial uses (and also as cooking fuel) and in modern stoves. The use of biomass for domestic heating could represent a significant mitigation potential. No quantitative estimates are available of future biomass demand for the built environment (for example, heating with pellets or cooking fuels) ( Chapter 6 ).

Biomass supplies

Biomass production on agricultural and degraded lands. Table 11.2 summarizes the biomass supply energy potentials discussed in Chapters 8 (agriculture), 9 (Forestry) and 10 (waste). Those potentials are accompanied by considerable uncertainties. In addition, the estimates are derived from scenarios for the year 2050 . The largest contribution could come from energy crops on arable land, assuming that efficiency improvements in agriculture are fast enough to outpace food demand so as to avoid increased pressure on forests and nature areas. Section 8.4.4.2 provides a range from 20–400 EJ. The highest estimate is a technical potential for 2050 . Technically, the potentials for such efficiency increases are very large, but the extent to which such potentials can be exploited over time is still poorly studied. Studies assume the successful introduction of biomass production in key regions as Latin America, Sub-Saharan Africa, Eastern Europe and Oceania, combined with gradual improvements in agricultural practice and management (including livestock). However, such development schemes – that could also generate substantial additional income for rural regions that can export biomass – are uncertain, and implementation depends on many factors such as trade policies, agricultural policies, the establishment of sustainability frameworks such as certification, and investments in infrastructure and conventional agriculture (see also Faaij & Domac, 2006 [NotFound] ).

In addition, the use of degraded lands for biomass production (as in reforestation schemes: 8–110 EJ) could contribute significantly. Although biomass production with such low yields generally results in more expensive biomass supplies, competition with food production is almost absent and various co-benefits, such as the regeneration of soils (and carbon storage), improved water retention, and protection from erosion may also offset some of the establishment costs. An important example of such biomass production schemes at the moment is the establishment of jatropha crops (oil seeds, also spelled jathropa) on marginal lands.

Biomass residues and wastes. Table 11.2 also depicts the energy potentials in residues from forestry (12–74 EJ/yr) and agriculture (15–70 EJ/yr) as well as waste (13 EJ/yr). Those biomass resource categories are largely available before 2030, but also somewhat uncertain. The uncertainty comes from possible competing uses (for example, the increased use of biomaterials such as fibreboard production from forest residues and the use of agro-residues for fodder and fertilizer) and differing assumptions about the sustainability criteria deployed with respect to forest management and agriculture intensity. The current energy potential of waste is approximately 8 EJ/yr, which could increase to 13 EJ in 2030 . The biogas fuel potentials from waste, landfill gas and digester gas are much smaller.

Table 11.2: Biomass supply potentials and biomass demand in EJ based on Chapters 4 to 10

| Sector | Supply | Demand | |||

|---|---|---|---|---|---|

| Biomass supplies to 2050 | Energy supply biomass demand 2030 | Transport biomass demand 2030 | Built environment | Industry | |

| Agriculture | Relevant, in particular in developing countries as cooking fuel | Sugar industry significant. Food & beverage industry. No quantitative estimate on use for new biomaterials (e.g. bio-plastics) not significant for 2030. | |||

| Residues | 15-70 | ||||

| Dung | 5-55 | ||||

| Energy crops on arable land and pastures | 20-300 | ||||

| Crops on degraded lands | 60-150 | ||||

| Forestry | 12-74 | Key application | Relevant for second-generation biofuels | Relevant | |

| Waste | 13 | Power and heat production | Possibly via gasification | Minimal | Cement industry |

| Industry | Process residues | Relevant; paper & pulp industry | |||

| Total supply primary biomass | 125-760 | ||||

| Total demand primary biomass | 70-130 | 28-43 (electricity) Heat excluded | 45-85 | Relevant (currently several dozens of EJ; additional demand may be limited) | Significant demand; paper & pulp and sugar industry use own process residues; additional demand expected to be limited |

Synthesis of biomass supply & demand

A proper comparison of demand and supply is not possible since most of the estimates for supply relate to 2050 . Demand has been assessed for 2030 . Taking this into account, the lower end of the biomass supply (estimated at about 125 EJ/yr) exceeds the lower estimate of biomass demand (estimated at 70 EJ/yr). However, demand does not include estimates of domestic biomass use (such as cooking fuel, although that use may diminish over time depending on development pathways in developing countries), increased biomass for production of heat (although additional demand in this area may be limited) and biomass use in industry (excluding the possible demand of biomass for new biomaterials). It seems that this demand can be met by biomass residues from forestry, agriculture, waste and dung and a limited contribution from energy crops. Such a ‘low biomass demand’ pathway may develop from the use of agricultural crops with more limited potentials, lower GHG mitigation impact and less attractive economic prospects, in particular in temperate climate regions. The major exception here is sugar-cane-based ethanol production.

The estimated high biomass demand consists of an estimated maximum use of biomass for power production and the constrained growth of production of biofuels when the WEO projections are taken into consideration (25 EJ/yr biofuels and about 40 EJ/yr primary biomass demand). Total combined demand for biomass for power and fuels adds up to about 130 EJ/yr. Clearly, a more substantial contribution from energy crops (perhaps in part from degraded lands, for example producing jatropha oil seeds) is required to cover total demand of this magnitude, but this still seems feasible, even for 2030; the low-end estimate for energy crops for agricultural land is 50 EJ/yr, which is in line with the 40 EJ/yr primary projected demand for biofuels.

However, as was also acknowledged in the WEO, the demand for biomass as biofuels in around 2030 will depend in particular on the commercialization of second-generation biofuel technologies (i.e. the large-scale gasification of biomass for the production of synfuels as Fischer-Tropsch diesel, methanol or DME, and the hydrolysis of lignocellulosic biomass for the production of ethanol). According to Hamelinck and Faaij 2006 [SRC] ), such technologies offer competitive biofuel production compared to oil priced at between 40–50 US$/barrel (assuming biomass prices of around 2 US$/GJ). In Chapter 5 , Figure 5.9 ( IEA, 2006b [NPR] ), however, assumes higher biofuel costs. Another key option is the wider deployment of sugar cane for ethanol production, especially on a larger scale using state-of-the art mills, and possibly in combination with hydrolysis technology and additional ethanol production from bagasse (as argued by ( Moreira, 2006 ) and other authors). The availability of such technologies before 2020 may lead to an acceleration of biofuel production and use, even before 2030 . Biofuels may therefore become the most important demand factor for biomass, especially in the longer term (i.e. beyond 2030 ).

A more problematic situation arises when the development of biomass resources (both residues and cultivated biomass) fails to keep up with demand. Although the higher end of biomass supply estimates ( 2050 ) is well above the maximum projected biomass demand for 2030, the net availability of biomass in 2030 will be considerably lower than the 2050 estimates. If biomass supplies fall short, this is likely to lead to significant price increases for raw materials. This would have a direct effect on the economic feasibility of various biomass applications. Generally, biomass feedstock costs can cover 30–50% of the production costs of secondary energy carriers, so increasing feedstock prices will quickly reduce the increase in biomass demand (but simultaneously stimulate investments in biomass production). To date, there has been very little research into interactions of this kind, especially at the global scale.

Comparing mitigation estimates for top-down and bottom-up modelling is not straightforward. Bottom-up mitigation responses are typically more detailed and derived from more constrained modelling exercises. Cost estimates are therefore in partial equilibrium in that input and output market prices are fixed, as may be key input quantities such as acreage or capital. Top-down mitigation responses consider more generic mitigation technologies and changes in outputs and inputs (such as shifts from food crops or forests to energy crops) as well as changes in market prices (such as land prices as competition for land increases). In addition, current top-down models optimistically assume the simultaneous global adoption of a coordinated climate policy with an unconstrained, or almost unconstrained, set of mitigation options across sectors. A review of top-down studies ( Chapter 3 data assembled from Rose et al. 2007 [NPR, MoS, ARC, 2007] and US CCSP 2006 [NPR] )) results in a range for total projected biomass use over all cost categories of 20 to 79 EJ/yr (defined as solid and liquid, requiring a conversion ratio from primary biomass to fuels). This is, on average, half the range for estimates obtained via bottom-up information from the various chapters.

Given the relatively small number of relevant scenario studies available to date, it is fair to say that the role of biomass in long-term stabilization (beyond 2030 ) will be very significant but that it is subject to relatively large uncertainties. Further research is required to improve our insight into the potential. A number of key factors influencing biomass mitigation potential are worth noting: the baseline economic growth and energy supply alternatives, assumptions about technological change (such as the rate of development of cellulosic ethanol conversion technology), land use competition, and mitigation alternatives (overall and land-related).

Given the lack of studies of how biomass resources may be distributed over various demand sectors, we do not suggest any allocation of the different biomass supplies to various applications. Furthermore, the net avoidance costs per ton of CO2 of biomass usage depend on a wide variety of factors, including the biomass resource and supply (logistics) costs, conversion costs (which in turn depend on the availability of improved or advanced technologies) and reference fossil fuel prices, most notably of oil.

11.3.1.5 Estimates of mitigation potentials from Chapters 4 to 10

Table 11.3 uses the procedures outlined above to bring together the estimates for the economic potentials for GHG mitigation from Chapters 4 to 10 . It was not possible to break down the potential into the desired cost categories for all sectors. Where appropriate, then, the cells in the table have been merged to account for the fact that the numbers represent the total of two cost categories. Only the potentials in the cost categories up to 100 US$/tCO2-eq are reported here. Some of the chapters also report numbers for the potential in higher cost categories. This is the case for Chapter 5 (transport) and Chapter 8 (agriculture).

Table 11.3 suggests that the economic potential for reducing GHG emissions at costs below 100 US$/tCO2 ranges [7] from 16 to 30 GtCO2-eq. The contributions of each sector to the totals are in the order of magnitude 2 to 6 GtCO2-eq (mid-range numbers), except for the waste sector (0.4 to 1 GtCO2-eq). The mitigation potentials at the lowest cost are estimated for the buildings sector. Based on the literature assessment presented in Chapter 6 it can be concluded that over 80% of the buildings potential can be identified at negative cost. However, significant barriers need to be overcome to achieve these potentials. See Chapter 6 for more information on these barriers.

In all sectors, except for the transport sector, the highest economic potential for emission reduction is thought to be in the non-OECD/EIT region. In relative terms, although it is not possible to be exact because baselines across sectors are different, the emission reduction options at costs below 100 US$/tCO2-eq are in the range of 30 to 50% of the totalled baseline. This is an indicative figure as it is compiled from a range of different baselines.

Table 11.3: Estimated economic potentials for GHG mitigation at a sectoral level in 2030 for different cost categories using the SRES B2 and IEA World Energy Outlook ( 2004 ) baselines

| Sector | Mitigation optiona) | Region | Economic potential <100 US$/tCO2-eqc) | Economic potential in different cost categoriesd), e) | ||||

|---|---|---|---|---|---|---|---|---|

| Cost cat. US$/tCO2-eq | <0 | 0-20 | 20-50 | 50-100 | ||||

| Cost cat. US$/tC-eq | <0 | 0-73 | 73-183 | 183-367 | ||||

| Low | High | |||||||

| Gt CO2-eq | ||||||||

|

Energy supplye) (see also 4.4) |

All options in energy supply excl. electricity savings in other sectors | OECD | 0.90 | 1.7 | 0.9 | 0.50 | 0 | |

| EIT | 0.20 | 0.25 | 0.15 | 0.06 | 0 | |||

| Non-OECD/EIT | 1.3 | 2.7 | 0.80 | 0.90 | 0.35 | |||

| Global | 2.4 | 4.7 | 1.9 | 1.4 | 0.35 | |||

|

Transportb), e), g) (see also 5.6) |

Total | OECD | 0.50 | 0.55 | 0.25 | 0.25 | 0 | 0 |

| EIT | 0.05 | 0.05 | 0.03 | 0 | 0 | 0.02 | ||

| Non-OECD/EIT | 0.15 | 0.15 | 0.10 | 0.03 | 0.02 | 0 | ||

| Globalb) | 1.6 | 2.5 | 0.35 | 1.4 | 0.15 | 0.15 | ||

|

Buildings (see also 6.4)f), h) |

Electricity savings | OECD | 0.8 | 1.0 | 0.95 | 0.00 | 0 | |

| EIT | 0.2 | 0.3 | 0.25 | 0 | 0 | |||

| Non-OECD/EIT | 2.0 | 2.5 | 2.1 | 0.05 | 0.05 | |||

| Fuel savings | OECD | 1.0 | 1.3 | 0.85 | 0.15 | 0.15 | ||

| EIT | 0.6 | 0.8 | 0.2 | 0.15 | 0.35 | |||

| Non-OECD/EIT | 0.7 | 0.8 | 0.65 | 0.10 | 0.01 | |||

| Total | OECD | 1.8 | 2.3 | 1.8 | 0.15 | 0.15 | ||

| EIT | 0.9 | 1.1 | 0.45 | 0.15 | 0.35 | |||

| Non-OECD/EIT | 2.7 | 3.3 | 2.7 | 0.15 | 0.10 | |||

| Global | 5.4 | 6.7 | 5.0 | 0.50 | 0.60 | |||

|

Industry (see also 7.5) |

Electricity savings | OECD | 0.30 | 0.07 | 0.07 | 0.15 | ||

| EIT | 0.08 | 0.02 | 0.02 | 0.040 | ||||

| Non-OECD/EIT | 0.45 | 0.10 | 0.10 | 0.25 | ||||

| Other savings, including non-CO2 GHG | OECD | 0.35 | 0.90 | 0.30 | 0.25 | 0.05 | ||

| EIT | 0.20 | 0.45 | 0.08 | 0.25 | 0.02 | |||

| Non-OECD/EIT | 1.2 | 3.3 | 0.50 | 1.7 | 0.08 | |||

| Total | OECD | 0.60 | 1.2 | 0.35 | 0.35 | 0.20 | ||

| EIT | 0.25 | 0.55 | 0.10 | 0.25 | 0.06 | |||

| Non-OECD/EIT | 1.6 | 3.8 | 0.60 | 1.8 | 0.30 | |||

| Global | 2.5 | 5.5 | 1.1 | 2.4 | 0.55 | |||

|

Agriculture (see also 8.4) |

All options | OECD | 0.45 | 1.3 | 0.30 | 0.20 | 0.30 | |

| EIT | 0.25 | 0.65 | 0.15 | 0.10 | 0.15 | |||

| Non-OECD/EIT | 1.6 | 4.5 | 1.1 | 0.75 | 1.2 | |||

| Global | 2.3 | 6.4 | 1.6 | 1.1 | 1.7 | |||

|

Forestry (see also 9.4) |

All options | OECD | 0.40 | 1.0 | 0.01 | 0.25 | 0.30 | 0.25 |

| EIT | 0.09 | 0.20 | 0 | 0.05 | 0.05 | 0.05 | ||

| Non-OECD/EIT | 0.75 | 3.0 | 0.15 | 0.90 | 0.55 | 0.35 | ||

| Global | 1.3 | 4.2 | 0.15 | 1.1 | 0.90 | 0.65 | ||

|

Waste (see also 10.4) |

All options | OECD | 0.10 | 0.20 | 0.10 | 0.06 | 0.00 | 0.00 |

| EIT | 0.10 | 0.10 | 0.05 | 0.05 | 0.00 | 0.00 | ||

| Non-OECD/EIT | 0.20 | 0.70 | 0.25 | 0.07 | 0.10 | 0.04 | ||

| Global | 0.40 | 1.0 | 0.40 | 0.18 | 0.10 | 0.04 | ||

|

All sectorsi) |

All options | OECD | 4.9 | 7.4 | 2.2 | 2.1 | 1.3 | 1.1 |

| EIT | 1.8 | 2.8 | 0.55 | 0.65 | 0.50 | 1.0 | ||

| Non-OECD/EIT | 8.3 | 16.8 | 3.3 | 3.6 | 4.1 | 2.4 | ||

| Global | 15.8 | 31.1 | 6.1 | 7.4 | 6.0 | 4.5 | ||

A number of comments should be made on the overview presented in Table 11.3 .

First, a set of emission reduction options have been excluded from the analysis, because the available literature did not allow for a reliable assessment of the potential. [8]

- Emission reduction estimates of fluorinated gases from energy supply, transport and buildings are not included in the sector mitigation potentials from Chapters 4 to 6 . For these sectors, the special IPCC report on ozone and climate (IPCC & TEAP, 2005) reported a mitigation potential for HFCs of 0.44 GtCO2-eq for the year 2015 (a mitigation potential of 0.46 GtCO2-eq was reported for CFCs and HCFCs).

- The potential for combined generation of heat and power in the energy supply sector has not added to the other potentials as it is uncertain (see Section 4.4.3 ). IEA (2006a) quotes a potential here of 0.2 to 0.4 GtCO2-eq.

- The potential emissions reduction for coal mining and gas pipelines has not been included in the reductions from the power sector. De Jager et al. (2001) indicated that the CH4 emissions from coal mining in 2020 might be in the order of 0.65 GtCO2-eq. Reductions of 70 to 90% with a penetration level of 40% might be possible, resulting for 2020 in the order of 0.20 GtCO2-eq. Higher reduction potentials of 0.47 GtCO2-eq for CH4 from coal mining have also been mentioned (Delhotal et al., 2006).

- Emission reductions in freight transport (heavy duty vehicles), public transport, and marine transport have not been included. In the transport sector, only the mitigation potential for light duty vehicle efficiency improvement (LDV), air planes and biofuels for road transport has been assessed. Because LDV represents roughly two-thirds of transportation by road, and because road transportation represents roughly three-quarters of transport as a whole (air, water, and rail transport represent roughly 11, 9 and 3 percent of overall transport respectively), the estimate for LDV broadly reflects half of the transport activity for which a mitigation potential of over 0.70 GtCO2-eq is reported. In the case of marine transport, the literature studies discussed in Section 5.3.4 indicate that large reductions are possible compared to the current standard but this might not be significant when comparing to a baseline. See also Table 5.8 for indicative potentials for some of the options.

- Non-technical options in the transport sector, like speed limits and changes in modal split or behaviour changes, are not taken into account (an indication of the order of magnitude for Latin American cities is given in Table 5.6 ).

- For the buildings sector, most literature sources focused on low-cost mitigation options and so high-cost options are less well represented. Behavioural changes in the buildings sector have not been included; some of these raise energy demand, examples being rebound effects from improvements in energy efficiency. [9]

- In the industry sector, the fuel savings have only been estimated for the energy-intensive sectors representing approximately 50% of fuel use in manufacturing industry.

- The TAR stated an emission reduction estimate of 2.20 GtCO2-eq in 2020 for material efficiency. Chapter 7 does not include material efficiency, except for recycling for selected industries, in the estimate of the industrial emission reduction potential. To avoid double counting, the TAR estimate should not be added to the potentials of Chapter 7 . However, it is likely that the potential for material efficiency significantly exceeds that for recycling for selected industries only given in Chapter 7 .

In conclusion, the options excluded represent significant potentials that justify future analysis. These options represent about 10 to 15% of the potential reported in Table 11.3 ; this magnitude is not such that the conclusions of the bottom-up analysis would change substantially.

Secondly, the chapters identified a number of key sensitivities that have not been quantified. Note that the key sensitivities are different for the different sectors.

In general, higher energy prices will have some impact on the mitigation potentials presented here (i.e. those with costs below 100 US$/tCO2-eq), but the impact is expected to be generally limited, except for the transport sector (see below). No major options have been identified exceeding 100 US$/tCO2-eq that could move to below 100 US$/tCO2-eq. However, this is only true of the fairly static approach presented here. The costs and potential of technologies in 2030 may be different if energy prices remain high for several decades compared to the situation if they return to the levels of the 1990 s. High energy prices may also impact the baseline since the fuel mix will change and lower emissions can be expected. Note that options in some areas, such as agriculture and forestry and non-CO2 greenhouse gases (about one third of the potential reported), are not affected by energy prices, or much less so.

More specifically, an important sensitivity for the transport sector is the future oil price. The total potential for the LDV in transport increases by 7% as prices rise from 30 to 60 US$/barrel. However, the potential at costs <0 US$/tCO2 increases much more – by almost 90% – because of the fuel saving effect. (See Section 5.4.2 ).

- Discount rates that formed the basis of the analysis are – as reported in the individual chapters – in the range of 3 to 10%, with the majority of studies using the lower end of this range. Lower discount rates (e.g. 2%) would imply some shift to lower cost ranges, without substantially affecting the total potential. Moving to higher discount rates would have a particular impact on the potential in the highest cost range, which makes up 15 to 20% of the total potential.

- Agriculture and forestry potential estimates are based on long-term experimental results under current climate conditions. Given moderate deviations in the climate expected by 2030, the mitigation estimates are considered quite robust.

Thirdly, potentials with costs below zero US$/tCO2-eq are presented in Table 11.3 . The potential at negative cost is considerable. There is evidence from business studies showing the existence of mitigation options at negative cost (for example, The Climate Group, 2005 ). For a discussion of the reasons for mitigation options at negative costs, see IPCC 2001 [NPR] ), Chapters 3 and 7 ; and Chapters 2 and 6 , and Section 11.6 of this report.

These remarks do not affect the validity of the overall findings, i.e. that the economic potential at costs below 100 US$/tCO2-eq ranges from 16 to 30 GtCO2-eq. However, they reflect a basic shortcoming of the bottom-up analysis. For individual countries, sectors or gases, the literature includes excellent bottom-up analysis of mitigation potentials. However, they are usually not comparable and their coverage of countries/sectors/gases is limited.

The following gaps in the literature have been identified. Firstly, there is no harmonized integrated standard for bottom-up analysis that compares all future economic potentials. Harmonization is considered important for, inter alia, target years, discount rates, price scenarios. Secondly, there is a lack of bottom-up estimates of mitigation potentials, including those for rebound effects of energy-efficiency policies for transport and buildings, for regions such as many EIT countries and substantial parts of the non-OECD/EIT grouping.

11.3.1.6 Comparison with the Third Assessment Report (TAR)

Table 11.4 compares the estimates in this report (AR4) for 2030 with those from the TAR for 2020, which were evaluated at costs less than 27 US$/tCO2-eq (100 US$/tCO2-eq). The last column shows the AR4 estimates for potentials at costs of less than 20 US$/tCO2-eq, which are more comparable with those from the TAR. Overall, the estimated bottom-up economic potential has been revised downwards compared to that in the TAR, even though this report has a longer time horizon than the TAR. Only the buildings sector has been revised upwards in this cost category. For the forestry sector, the economic potential now is significantly lower compared to TAR. However, the TAR numbers for the forestry potential were not specified in terms of cost levels and are more comparable with the < 100 US$/tCO2-eq potential in this report. Even then, they are much higher because they are based on top-down global forest models. These models generally give much higher values then bottom-up studies, as reflected in Chapter 9 of this report. The industry sector is estimated to have a lower potential at costs below 20 US$/tCO2-eq, partly due to a lack of data available for use in the AR4 analyses. Only electricity savings have been included for light industry. In addition, the potential for CHP was allocated to the industry sector in the TAR and was not covered in this report. The most important difference between the TAR and the current analysis is that, in the TAR, material efficiency in a wide sense has been included in the industry sector. In this report, only some aspects of material efficiency have been included, namely in Chapter 7 .

Table 11.4: Comparison of potential global emission reductions for 2030 with the global estimates for 2020 from the Third Assessment Report (TAR) in GtCO2-eq

| Sector | Options | TAR potential emissions reductions by 2020 at costs <27.3 US$/tCO2 a) | AR4 potential emissions reductions by 2030 at costs <20 US$/tCO2 b) | ||

|---|---|---|---|---|---|

| Estimate | Low | High | Low | High | |

| Energy supply and conversion | 1.3 | 2.6 | 1.2 | 2.4 | |

| Transport | CO2 only | 1.1 | 2.6 | 1.3 | 2.1 |

| Buildings | CO2 only | 3.7 | 4.0 | 4.9 | 6.1 |

| Industry | 0.70 | 1.5 | |||

| - energy efficiency | 2.6 | 3.3 | |||

| - material efficiency | 2.2 | 2.2 | |||

| non-CO2 | 0.37 | 0.37 | |||

| Agriculturec) | C-sinks and non CO2 c) | 1.3 | 2.8 | 0.30 | 2.4 |

| Forestry | (11.7)d) | (11.7) | 0.55 | 1.9 | |

| Waste | CH4 only | 0.73 | 0.73 | 0.35 | 0.85 |

| Total | 13.2e) | 18.5e) | 9.3 | 17.1 | |

The updated estimates might be expected to be higher due to:

- The greater range of economic potentials, extending up to 100 US$/tCO2, compared to less than 27.3 US$/tCO2 (100 US$/tC) in the TAR;

- The different time frame: 2030 compared to 2020 in the TAR.

However, the overall estimated bottom-up economic potential has been revised downwards somewhat, compared to that in the TAR, especially considering that the AR4 estimates allow for about five more years of technological change. Part of the difference is caused by the lower coverage of mitigation options up to 2030 in the AR4 literature.

11.3.1.7 Conclusions of bottom-up potential estimates

When comparing the emission reduction potentials as presented in Table 11.4 with the baseline emissions, it can be concluded that the total economic potential at costs below 20 US$/tCO2-eq ranges from 15 to 30% of the total added-up baseline. The economic potential up to 100 US$/tCO2-eq is about 30 to 50% of emissions in 2030 . There is medium evidence for these conclusions because, although a significant amount of literature is available, there are gaps and regional biases, and baselines are different. There is also medium agreement on these conclusions because there is literature for each sector with substantial ranges but the ranges may not capture all the uncertainties that exist. Although there are differences in relative mitigation potentials and specific mitigation costs between sectors (e.g. the buildings sector has a large share of low-cost options), it is clear that the total mitigation potential is spread across the various sectors. Substantial emission reductions can only be achieved if most of the sectors contribute to the emission reduction. In addition, there are barriers that need to be overcome if these potentials are to materialize.

11.3.2 Comparing bottom-up and top-down sectoral potentials for 2030

Table 11.5 and Figure 11.3 bring together the ranges of economic potentials synthesized from Chapters 4 to 10 , as discussed in 11.3.1, with the ranges of top-down sectoral estimates for 2030 presented in Chapter 3 . The bottom-up estimates are shown with the potentials from end-use electricity savings attributed (1) to the end-use sectors, i.e. to the buildings and industry sectors primarily responsible for the electricity use and (2) upstream, at the point of emission to the energy supply sector. The top-down ranges are provided by an analysis of the data from multi-gas studies for 2030 reported in Section 3.6 . A relationship has been estimated between the absolute reductions in total GHGs and the carbon prices required to achieve them (see Appendix 3.1). Ranges for mitigation potential have been calculated for a 68% confidence interval for carbon prices at 20 and 100 US$( 2000 )/tCO2-eq. The ranges are shown in the last two columns of Table 11.5 .

Figure 11.3: Economic mitigation potential in different cost categories as compared to the baseline

of the economic potential range reported.

Table 11.5.: Economic potential for sectoral mitigation by 2030 : comparison of bottom-up and top-down estimates

| Chapter of report | Sector-based (‘bottom-up’) potential by 2030 (GtCO2-eq/yr) | Economy-wide model (‘top-down’) snapshot of mitigation by 2030 (GtCO2-eq/yr) | |||||

|---|---|---|---|---|---|---|---|

| Downstream (indirect) allocation of electricity savings to end-use sectors | Point-of-emissions allocation (emission savings from end-use electricity savings allocated to energy supply sector) | ||||||